Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

Open to apply: 16 Jan 2024

Close to apply: 23 Jan 2024

Balloting: 26 Jan 2024

Listing date: 07 Feb 2024

Close to apply: 23 Jan 2024

Balloting: 26 Jan 2024

Listing date: 07 Feb 2024

Share Capital

Market cap: RM151.503 mil

Total Shares: 432.866 mil shares

Market cap: RM151.503 mil

Total Shares: 432.866 mil shares

Industry (CAGR 2018-2022)

Malaysia external trade activities: 11.5%

The Philippines external trade activities: 3.3%

Korea external trade activities: 3.1%

Singapore external trade activities: 6.3%

Industry competitors comparison (net profit%)

1. AGX Group: 5.8%

2. Harbour: 17.4% (PE3.7)

3. Trimode: 8.4% (PE15.85)

4. Swift: 7.6% (PE8.53)

5. Others Listed companies in Malaysia: -13.5% to 6.1%

6. Other Listed companies in the Philippines: -39.3% to -3.6%

7. Other Listed companies in Korea, Myammar, Singapore: -47.3% to 7.1%

Malaysia external trade activities: 11.5%

The Philippines external trade activities: 3.3%

Korea external trade activities: 3.1%

Singapore external trade activities: 6.3%

Industry competitors comparison (net profit%)

1. AGX Group: 5.8%

2. Harbour: 17.4% (PE3.7)

3. Trimode: 8.4% (PE15.85)

4. Swift: 7.6% (PE8.53)

5. Others Listed companies in Malaysia: -13.5% to 6.1%

6. Other Listed companies in the Philippines: -39.3% to -3.6%

7. Other Listed companies in Korea, Myammar, Singapore: -47.3% to 7.1%

Business (FPE 2023)

Third-party logistics service provider.

Revenue by Segments

1. Sea freight forwarding: 36.76%

2. Air frieght forwarding: 17.11%

3. Aerospace logistics: 37.06%

4. Warehousing and other 3PL services: 5.68%

5. Road freight transportation: 3.39%

Revenue by Geographic market

1. Malysia: 16.43%

2. Philippines: 41.67%

3. Korea: 7.74%

4. Myanmar: 4.97%

5. Singapore: 10.48%

6. others: 18.71%

Third-party logistics service provider.

Revenue by Segments

1. Sea freight forwarding: 36.76%

2. Air frieght forwarding: 17.11%

3. Aerospace logistics: 37.06%

4. Warehousing and other 3PL services: 5.68%

5. Road freight transportation: 3.39%

Revenue by Geographic market

1. Malysia: 16.43%

2. Philippines: 41.67%

3. Korea: 7.74%

4. Myanmar: 4.97%

5. Singapore: 10.48%

6. others: 18.71%

Fundamental

1.Market: Ace Market

2.Price: RM0.35

3.Forecast P/E: 12.68 (latest 12 month, EPS RM0.0276)

4.ROE(Pro forma III): 15.17%

5.ROE: 22.82%(FPE2023),29.87%(FYE2022), 15.14%(FYE2021), 18.53%(FYE2020),

6.Net asset: RM0.18

7.Total debt to current asset: 0.071 (Debt: 6.682mil, Non-Current Asset: 19.488mil, Current asset: 93.751mil)

8.Dividend policy: 30% PAT dividend policy.

9. Shariah status: Yes

1.Market: Ace Market

2.Price: RM0.35

3.Forecast P/E: 12.68 (latest 12 month, EPS RM0.0276)

4.ROE(Pro forma III): 15.17%

5.ROE: 22.82%(FPE2023),29.87%(FYE2022), 15.14%(FYE2021), 18.53%(FYE2020),

6.Net asset: RM0.18

7.Total debt to current asset: 0.071 (Debt: 6.682mil, Non-Current Asset: 19.488mil, Current asset: 93.751mil)

8.Dividend policy: 30% PAT dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2023 (FPE 31Aug, 8mths): RM122.228 mil (Eps: 0.0172), PAT: 6.09%

2022 (FYE 31Dec): RM234.429 mil (Eps: 0.0313), PAT: 5.78%

2021 (FYE 31Dec): RM193.372 mil (Eps: 0.0137),PAT: 3.07%

2020 (FYE 31Dec): RM122.507 mil (Eps: 0.0013),PAT: 0.46%

2023 (FPE 31Aug, 8mths): RM122.228 mil (Eps: 0.0172), PAT: 6.09%

2022 (FYE 31Dec): RM234.429 mil (Eps: 0.0313), PAT: 5.78%

2021 (FYE 31Dec): RM193.372 mil (Eps: 0.0137),PAT: 3.07%

2020 (FYE 31Dec): RM122.507 mil (Eps: 0.0013),PAT: 0.46%

Major customer (FPE 2023)

1.Airasia Group: 27.37%

2.Kukdo Chemical Co.,Ltd: 7.16%

3.Autoliv Cebu Safety Manufacturing Inc: 3.49%

4.Moog Controls Corporation: 3.29%

5.Customer Group B: 2.83%

***total 44.15%

1.Airasia Group: 27.37%

2.Kukdo Chemical Co.,Ltd: 7.16%

3.Autoliv Cebu Safety Manufacturing Inc: 3.49%

4.Moog Controls Corporation: 3.29%

5.Customer Group B: 2.83%

***total 44.15%

Major Sharesholders

1. Dato’ Ponnudorai A/L Periasamy: 11.54%

2. Jayasielan A/L Gopal: 11.54%

3. Penu Mark: 17.6%

4. Neo Lip Pheng, Peter: 17.6%

5. Maximino Baylen Gulmayo, Jr.: 4.97%

1. Dato’ Ponnudorai A/L Periasamy: 11.54%

2. Jayasielan A/L Gopal: 11.54%

3. Penu Mark: 17.6%

4. Neo Lip Pheng, Peter: 17.6%

5. Maximino Baylen Gulmayo, Jr.: 4.97%

Directors & Key Management Remuneration for FYE2023

(from Revenue & other income 2022)

Total director remuneration: RM3.413 mil

key management remuneration: RM1.5 mil – RM1.65 mil

total (max): RM5.063 mil or 10.04%

(from Revenue & other income 2022)

Total director remuneration: RM3.413 mil

key management remuneration: RM1.5 mil – RM1.65 mil

total (max): RM5.063 mil or 10.04%

Use of funds

1.Business expansion: 25.8%

2.Repayment of bank borrowings: 12.2%

3.Working capital: 48.7%

4.Estimated listing expenses: 13.3%

1.Business expansion: 25.8%

2.Repayment of bank borrowings: 12.2%

3.Working capital: 48.7%

4.Estimated listing expenses: 13.3%

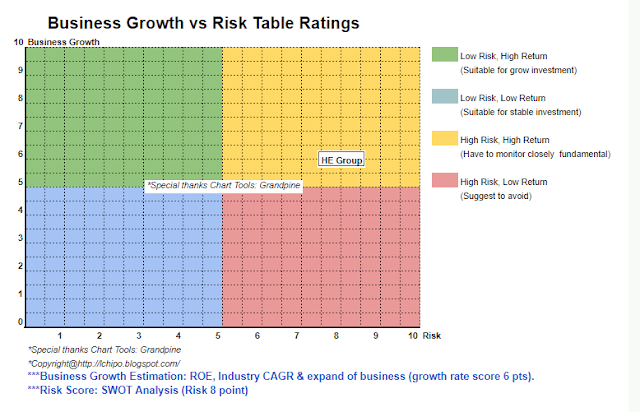

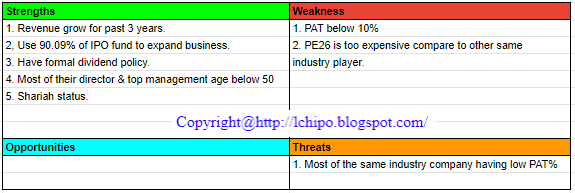

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is high risk investment.

Overall is high risk investment.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.