Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 25/11/2022

Close to apply: 01/11/2022

Balloting: 05/12/2022

Listing date: 13/12/2022

Close to apply: 01/11/2022

Balloting: 05/12/2022

Listing date: 13/12/2022

Share Capital

Market cap: mil (will depend on final IPO price)

Total Shares: 1.028bil shares

Industry CARG (2017-2021)

GVA of Digital Economy: 6%

Competitors Netprofit margin%

ITMAX Group: 36.7%

EV-Dynamic S/B: 1.7%

Signify Malaysia S/B: 1.6%

TNB Research S/B: 3.5%

ITRAMAS Corporation S/B: 2.0%

Industronics Bhd: -11.8%

Turbine Technique (M) S/B: 9.9%

Norangkasa Enterprise S/B: 1.0%

VADS Lyfe S/B: 40.4%

Business (FYE 2022)

Supply and installation and provision of public space networked systems.

(Networked lighting systems, networked traffic management system, Networked video survelliance facilities, & other for local gov & ministry, telecommuications services providers.)

Revenue by Geo

Msia: 100% (Selangor, KL, Sabah)

Supply and installation and provision of public space networked systems.

(Networked lighting systems, networked traffic management system, Networked video survelliance facilities, & other for local gov & ministry, telecommuications services providers.)

Revenue by Geo

Msia: 100% (Selangor, KL, Sabah)

Fundamental

1.Market: Main Market

2.Price: RM1.07

3.P/E: 37.7 @ RM0.0284 (PE will difference if final IPO price is not RM1.07)

4.ROE(Pro Forma III): 12.03%

5.ROE: 54.22%(FYE2021), 41.28%(FYE2020), 8.83%(FYE2019)

6.NA after IPO: RM0.25

7.Total debt to current asset after IPO: 0.456 (Debt: 115.185mil, Non-Current Asset: 119.718mil,

1.Market: Main Market

2.Price: RM1.07

3.P/E: 37.7 @ RM0.0284 (PE will difference if final IPO price is not RM1.07)

4.ROE(Pro Forma III): 12.03%

5.ROE: 54.22%(FYE2021), 41.28%(FYE2020), 8.83%(FYE2019)

6.NA after IPO: RM0.25

7.Total debt to current asset after IPO: 0.456 (Debt: 115.185mil, Non-Current Asset: 119.718mil,

Current asset: 252.331mil)

8.Dividend policy: target 20% PAT dividend policy.

9. Shariah starus: Yes

9. Shariah starus: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 30Jun, 6mths): RM40.740 mil (Eps: 0.01503),PAT: 37.9%

2021 (FYE 31Dec): RM79.759 mil (Eps: 0.02844),PAT: 36.7%

2020 (FYE 31Dec): RM47.538 mil (Eps: 0.01232),PAT: 26.7%

2019 (FYE 31Dec): RM37.212 mil (Eps: 0.00153),PAT: 4.2%

Major customer (2022)

1. DBKL: 94.5%

2. Norangkasa Enterprise Sdn Bhd: 2.0%

3. Bank Rakyat: 0.9%

4. Wbe Digital Sdn Bhd: 0.6%

5. Ahmad Zaki Sdn Bhd: 0.5%

***total 98.5%

***DBKL Remaining order book: 438mil (until 2029), 10.757mil(until 2023), 60.740mil(until2023)

Major Sharesholders

Tan Sri Dato’ (Dr.) Tan Boon Hock: 51.3% (indirect)

Datin Afinaliza: 17.6% (indirect)

Tan Wei Lun: 51.3% (indirect)

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM1.443mil

key management remuneration: RM0.80mil - RM0.95mil

total (max): RM2.393 mil or 4.48%

Tan Sri Dato’ (Dr.) Tan Boon Hock: 51.3% (indirect)

Datin Afinaliza: 17.6% (indirect)

Tan Wei Lun: 51.3% (indirect)

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM1.443mil

key management remuneration: RM0.80mil - RM0.95mil

total (max): RM2.393 mil or 4.48%

Use of funds

1. Smart city application expansion to other local governments, federal ministries, and existing customers: 41.7%

2. Expansion of R&D capabilities: 6.1%

3. Expansion into enterprise market: 9.8%

4. Network and telecommunication infrastructure expansion: 19.4%

5. Working capital: 14.3%

6. Repayment of borrowings: 3.9%

7. Listing Expenses: 4.8%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

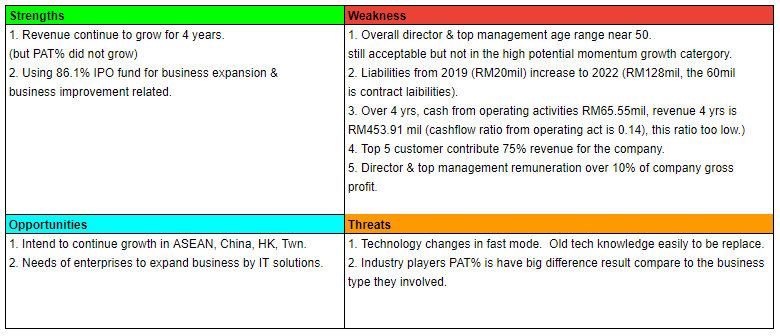

Overall is a non-discount IPO. The company have opportunities to grow but investor also must aware on the issue of over depend into single customer DBKL. (please refer to the above SWOT analysis table).

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Overall is a non-discount IPO. The company have opportunities to grow but investor also must aware on the issue of over depend into single customer DBKL. (please refer to the above SWOT analysis table).

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.