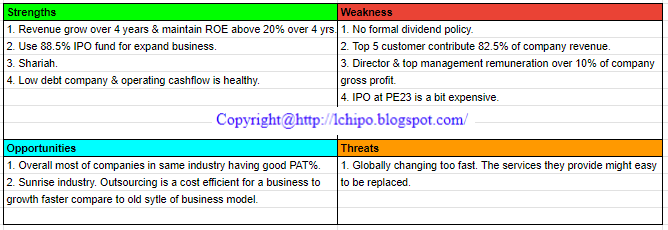

Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

Open to apply: 28 June 2023

Close to apply: 07 July 2023

Balloting: 11 July 2023

Listing date: 20 July 2023

Close to apply: 07 July 2023

Balloting: 11 July 2023

Listing date: 20 July 2023

Share Capital

Market cap: RM664.903mil

Total Shares: 820,868,600 shares

Market cap: RM664.903mil

Total Shares: 820,868,600 shares

Industry CARG (2018-2022)

Malaysia’s import value of golf equipment: 2.5% (total growth)

Malaysia’s export value of golf equipment: 1.9% (total growth)

Singapore’s import value of golf equipment: 19.4% (total growth)

Singapore’s export value of golf equipment: 12.6% (total growth)

Industry competitors comparison (net profit%)

MST Golf Group: 9.7%

Winston’s S/B: 16.7%

RGT Technology S/B: 11.3%

Desa Golf House S/B: 8.1%

Pan-West Pte Ltd: 4.4%

Vin Sporting House S/B: 3.0%

Leonian Singapore Pte Ltd: 2.1%

Golfsmart (M) S/B: 1.0%

SKT Ventures S/B: -1.9%

Malaysia’s import value of golf equipment: 2.5% (total growth)

Malaysia’s export value of golf equipment: 1.9% (total growth)

Singapore’s import value of golf equipment: 19.4% (total growth)

Singapore’s export value of golf equipment: 12.6% (total growth)

Industry competitors comparison (net profit%)

MST Golf Group: 9.7%

Winston’s S/B: 16.7%

RGT Technology S/B: 11.3%

Desa Golf House S/B: 8.1%

Pan-West Pte Ltd: 4.4%

Vin Sporting House S/B: 3.0%

Leonian Singapore Pte Ltd: 2.1%

Golfsmart (M) S/B: 1.0%

SKT Ventures S/B: -1.9%

Business (FYE 2022)

Retailer and wholesaler of golf equipment comprising golf clubs, golf balls and accessories and golf apparel in Malaysia and Singapore.

Revenue by Geo (FYE2022)

Malaysia: 66.30%

Singapore: 22.96%

Others: 10.74%

Retailer and wholesaler of golf equipment comprising golf clubs, golf balls and accessories and golf apparel in Malaysia and Singapore.

Revenue by Geo (FYE2022)

Malaysia: 66.30%

Singapore: 22.96%

Others: 10.74%

Fundamental

1.Market: Main Market

2.Price: RM0.81

3.P/E: 25 (EPS 0.0325 @ FYE2022)

4.ROE(Pro Forma III): 13.32%

5.ROE: 30.34%(FYE2022), 45.42%(FYE2021), 35.78%(FYE2020), 41.85%(FYE2019)

6.Net asset: RM0.27

7.Total debt to current asset IPO: 0.689 (Debt: 150.614mil, Non-Current Asset: 159.577mil, Current asset: 218.572mil)

8.Dividend policy: 30% PAT dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 31 Dec): RM300.875 mil (Eps: 0.0325),PAT: 9.68%

2021 (FYE 31Dec): RM206.519 mil (Eps: 0.0219),PAT: 9.73%

2020 (FYE 31Dec): RM170.152 mil (Eps: 0.0157),PAT: 8.05%

2019 (FYE 31Dec): RM175.950 mil (Eps: 0.0114),PAT: 5.81%

Operating cashflow vs PBT

2022: 23.05%

2021: 27.10%

2020: 281.11%

2019: 65.88%

Major customer (2022)

Do not have any major customer contribute more than 5% of company revenue.

***total -%

Major Sharesholders

1. All Sportz: 52.14% (direct)

2. Ng Yap Sio: 7.11% (direct)

3. Low Kok Poh: 3.56% (direct)

Directors & Key Management Remuneration for FYE2023

(from Revenue & other income 2022)

Total director remuneration: RM3.535mil

key management remuneration: RM1.3mil – RM1.5mil

total (max): RM5.03mil or 3.89%

Use of funds

1. Expansion in Malaysia and Singapore: 48.42%

2. Expansion into new geographical markets: 41.32%

3. Upgrade of digital technology facilities: 2.32%

4. Working capital requirements: 2.51%

5. Listing Expenses: 5.43%

Overall growth rating is 3.5 point because the industry itself having low CARG. Low industry CARG mean the market itself did not growth much, hence the growth of MST need to grab the market shares from competitor (instead of all competitor enjoy of expand of industry-cake size expand bigger concept).

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.