Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Disclaimer***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 18/09/2024

Close to apply: 25/09/2024

Balloting: 30/09/2024

Listing date: 09/10/2024

Share Capital

Market cap: RM302.9593 mil

Total Shares: 865.598 mil shares

Industry CARG

Imaging, analysis and testing industry size, Malaysia, 2019 – 2023: 8.37%

E&E industry size, Malaysia, 2019 – 2023: 9.0%

Semiconductor industry size, Malaysia, 2019 – 2023: 11.77%

Industry competitors comparison (net profit%)

1. Crest Group: 10.71%

2. CLMO technology Sdn Bhd: 15.99%

3. MTSC Solution Sdn Bhd: 17.92%

4. QES Group Berhad: 7.96% (PE28.95)

5. Others: 0.73% to 3.64%

Business (FPE 2024)

Provision of imaging, analytical and test solutions used primarily for quality inspection, sample analysis and R&D. (for industries like semiconductor, E&E, academic, automotive, oil and gas, aviation, life sciences and healthcare.)

Revenue by segment

1. Provision of imaging, analytical and test solutions: 81.06%

2. Provision of after-sales services: 18.94%

Revenue by Geo

1. Malaysia: 51.3%

2. Thailand: 17.4%

3. PRC: 19.3%

4. Singapore: 5.2%

5. Others: 6.8%

Fundamental

1.Market: Ace Market

2.Price: RM0.35

3.Forecast P/E: 16.59

4.ROE(Pro Forma): 19.5% (forecast)

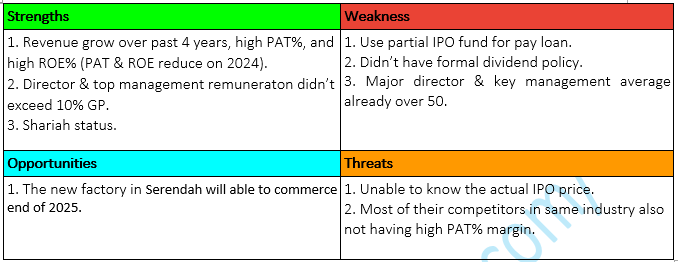

5.ROE: 34.06%(FYE2023), 33.14%(FYE2022), 30.21%(FYE2021), 22.29% (FYE2020)

6.Net asset: 0.11

7.Total debt to current asset: 0.327 (Debt: 45.956mil, Non-Current Asset: 6.677mil, Current asset: 140.713mil)

8.Dividend policy: 30% PAT dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2024 (FPE, 30Apr, 4mths): RM49.523 mil (Eps: 0.0035), PAT: 5.90%

2023 (FPE 31Dec): RM187.619 mil (Eps: 0.0238), PAT: 10.7%

2022 (FYE 31Dec): RM170.202 mil (Eps: 0.0208), PAT: 10.6%

2021 (FYE 31Dec): RM148.410 mil (Eps: 0.0202),PAT: 11.7%

2020 (FYE 31Dec): RM124.425 mil (Eps: 0.0154),PAT: 10.9%

***Prospectuses book didn’t use enlarged shares after IPO for EPS calculation, hence we apply our own calculation for EPS result).

Major customer (FPE2024)

1. Customer group E: 9.61%

2. Customer group I: 4.44%

3. Customer group J: 4.11%

4. Chulabhorn Research Institute: 4.09%

5. Thai Tohken Thermo Co Ltd: 3.69%

***total 25.94%

Major Sharesholders

1. Climan: 55.00% (direct)

2. Lim Siong Wai: 5.98% (direct), 55% (Indirect)

3. Au Chun Mun: 5.65% (direct), 55% (Indirect)

4. Yap Kian Meng: 5.65% (direct), 55% (Indirect)

Directors & Key Management Remuneration for FYE2024

(from Revenue & other income 2023)

Total director remuneration: RM2.914 mil

key management remuneration: RM1.15 mil – RM1.35 mil

total (max): RM4.264 mil or 7.97%

Use of funds

1. Setup of a new centralised headquarters: 15.762mil, 34.45%

2. Business expansion: 14.517mil, 31.73%

3. Purchase of additional demonstration equipment: 5.868mil, 12.83%

4. Expansion of technical support and maintenance team: 3.6mil, 7.87%

5. Estimated listing expenses: 6mil, 13.12%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)Overall is middle to high risk investment, and also come with grow opportunities.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.