Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 06/07/2022

Close to apply: 13/07/2022

Balloting: 18/07/2022

Listing date: 26/07/2022

Close to apply: 13/07/2022

Balloting: 18/07/2022

Listing date: 26/07/2022

Share Capital

Market cap: RM119.651 mil

Total Shares: 373.910 mil shares

Industry CARG (2016-2020)

Msia Healthcare expenditure CARG: 6.7%

Competitors Comparison (PAT margin%)

UMC group:14.9%

Insan Damai S/B: 5.7%

Schiller Asia Pacific S/B: 6.5%

Stryker Corporation S/B: 3.3%

Teepham Medical S/B: 3.7%

Business (FYE 2021)

-Marketing and distribution of various branded medical devices and consumables & after-sales service for all products.

-Developing, manufacturing and marketing of our medical consumables

Revenue by Geo

Msia: 88.29%

Others countries: 11.71%

-Marketing and distribution of various branded medical devices and consumables & after-sales service for all products.

-Developing, manufacturing and marketing of our medical consumables

Revenue by Geo

Msia: 88.29%

Others countries: 11.71%

Fundamental

1.Market: Ace Market

2.Price: RM0.32

3.P/E: 13.11 @ RM0.0122

4.ROE(Pro Forma III): 9.22% (ProForma)

5.ROE: 32.32%(FYE2021), 36.47%(FYE2020), 24.99%(FYE2019)

6.NA after IPO: RM0.019

7.Total debt to current asset after IPO: 0.457 (Debt: 19.590mil, Non-Current Asset: 26.337mil, Current asset: 42.856mil)

8.Dividend policy: didn't have formal dividend policy.

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FPE 31Jan 6mths): RM36.855 mil (Eps: 0.0122),PAT: 12.41%

2021 (FYE 31Jul): RM34.116 mil (Eps: 0.0136),PAT: 14.91%

2020 (FYE 31Jul): RM23.676 mil (Eps: 0.0065),PAT: 10.22%

2019 (FYE 31Jul): RM16.422 mil (Eps: 0.0035),PAT: 8.03%

Major customer (2021)

1. Customer K: 8.47%

2. Customer A: 6.50%

3. Customer H: 4.99%

4. Customer L: 3.73%

5. Customer M: 3.61%

***total 27.3%

Major Sharesholders

UMediC Capital: 51.44% (direct)

Dato' Ng Chai Eng: 51.52% (indirect)

Lim Taw Seong: 51.44% (indirect)

Lau Chee Kheong: 51.44%

Directors & Key Management Remuneration for FYE2022 (from Revenue & other income 2021)

Total director remuneration: RM0.406 mil

key management remuneration: RM0.756 mil - RM1.050 mil

total (max): RM1.456 mil or 11.59%

Use of fund

1. Construction of new factory building (30mths): 11.25%

2. Setting up new marketing & distribution offices (36mths): 21.86%

3. Repayment bank borrowing: 28.93%

4. Working capital: 27.84%

5. Listing Expenses: 10.12%

Total director remuneration: RM0.406 mil

key management remuneration: RM0.756 mil - RM1.050 mil

total (max): RM1.456 mil or 11.59%

Use of fund

1. Construction of new factory building (30mths): 11.25%

2. Setting up new marketing & distribution offices (36mths): 21.86%

3. Repayment bank borrowing: 28.93%

4. Working capital: 27.84%

5. Listing Expenses: 10.12%

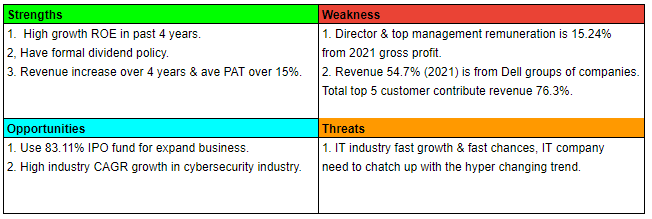

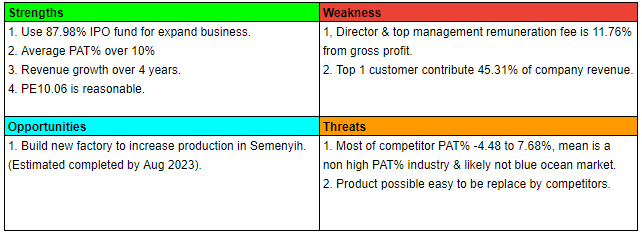

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is slightly better compare to other normal IPO. Kindly refer to the SWOT chart.

Overall is slightly better compare to other normal IPO. Kindly refer to the SWOT chart.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.