Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 15/06/2022

Close to apply: 21/06/2022

Balloting: 24/06/2022

Listing date: 05/07/2022

Close to apply: 21/06/2022

Balloting: 24/06/2022

Listing date: 05/07/2022

Share Capital

Market cap: RM76.839 mil

Total Shares: 247.868 mil shares

Industry & Competitor (PAT%)

Coffee, tea, milk and cocoa beverage industry size, 2018 – 2021 CAGR: 7.73%

Orgabio: 12.94%

Ori Bionature (M) S/B: 17.58%

AIM Food Manufacturing S/B: 11.46%

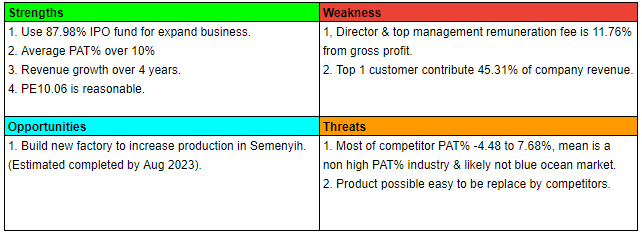

Others:-4.48% to 7.68%

Business (FPE 2022)

Instant beverage premix manufacturing services to third party brand owners and manufacturing, sales and marketing of house brand instant beverage premixes.

Revenue by Geo

M'sia: 78.10%

Papua New Guinea: 11.34%

S'pore: 2.04%

China: 3.84%

Trinidad and Tobago: 3.44%

Others: 1.24%

Fundamental

1.Market: Ace Market

2.Price: RM0.31

3.P/E: 10.06 @ EPS0.0308

4.ROE(Pro Forma III): 11.43% (ProForma)

5.ROE: 36.79%(FYE2021), 37.25%(FYE2020), 15.61%(FYE2019), 45%(FYE2018)

6.NA after IPO: RM0.19

7.Total debt to current asset after IPO: 0.75 (Debt: 24.771mil, Non-Current Asset: 39.306mil, Current asset: 32.812mil)

8.Dividend policy: No any formal dividend policy.

1.Market: Ace Market

2.Price: RM0.31

3.P/E: 10.06 @ EPS0.0308

4.ROE(Pro Forma III): 11.43% (ProForma)

5.ROE: 36.79%(FYE2021), 37.25%(FYE2020), 15.61%(FYE2019), 45%(FYE2018)

6.NA after IPO: RM0.19

7.Total debt to current asset after IPO: 0.75 (Debt: 24.771mil, Non-Current Asset: 39.306mil, Current asset: 32.812mil)

8.Dividend policy: No any formal dividend policy.

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FPE 31Dec, 6mths): RM34.843 mil (Eps: 0.0109),PAT: 7.77%

2021 (FYE 30Jun): RM59.072 mil (Eps: 0.0308),PAT: 12.94%

2020 (FYE 30Jun): RM39.373 mil (Eps: 0.0227),PAT: 14.31%

2019 (FYE 30Jun): RM31.696 mil (Eps: 0.0091),PAT: 7.14%

2018 (FYE 30Jun): RM32.670 mil (Eps: 0.0222),PAT: 16.85%

Factory ulilisation rate

2022: 73.58%

2021: 84.26%

2020: 70.44%

2019: 70.04%

2018: 83.18%

2022 (FPE 31Dec, 6mths): RM34.843 mil (Eps: 0.0109),PAT: 7.77%

2021 (FYE 30Jun): RM59.072 mil (Eps: 0.0308),PAT: 12.94%

2020 (FYE 30Jun): RM39.373 mil (Eps: 0.0227),PAT: 14.31%

2019 (FYE 30Jun): RM31.696 mil (Eps: 0.0091),PAT: 7.14%

2018 (FYE 30Jun): RM32.670 mil (Eps: 0.0222),PAT: 16.85%

Factory ulilisation rate

2022: 73.58%

2021: 84.26%

2020: 70.44%

2019: 70.04%

2018: 83.18%

Major customer (2021)

1. TDC Avenue Sdn Bhd: 45.31%

2. Hai-O Enterprise Bhd: 19.28%

3. Lotuss Stores (M) S/B: 2.83%

4. Amway (M) S/B: 1.19%

5. Eonsave: 0.95%

Total top 5 customer is 69.56% (2022)

Major Sharesholders:

Ean Yong & Sons: 61% (direct)

Hai-O: 10% (direct)

Directors & Key Management Remuneration for FYE2022 (from Revenue & other income 2021)

Total director remuneration: RM1.051 mil

key management remuneration: RM0.45 mil - RM0.0.60 mil

total (max): RM2.101 mil or 11.76%

Use of fund

1. Contruction of new factory: 53.39%

2. Acquisition of machinery: 7.44%

3. Working capital: 27.15%

4. Listing Expenses: 12.02%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a normal IPO. With the expand to build new factory should able to see increase of revenue after new factory start operate Aug 2023.

Overall is a normal IPO. With the expand to build new factory should able to see increase of revenue after new factory start operate Aug 2023.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.