Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

Open to apply: 29/12/2022

Close to apply: 06/01/2023

Balloting: 10/01/2023

Listing date: 18/01/2023

Close to apply: 06/01/2023

Balloting: 10/01/2023

Listing date: 18/01/2023

Share Capital

Market cap: RM159.12mil

Total Shares: 468mil shares

Industry CARG (2017-2021)

Global semiconductor sales CAGR: 7.8%

Global optoelectronic sales: 5.7%

Global solar cell and module production: 23.2%

Global semiconductor manufacturing equipment sales: 16%

Industry competitors comparison (net profit%)

TTVHB: 17.6% (PE15.19)

Vitrox: 24.9% (PE36.44)

Penta: 22.7% (PE39.33)

Mi: 16% (PE18)

Genetec: 26% (PE21.69)

AT: -163.7% (PE-0.59)

Aimflex: 6.2% (PE15.15)

Visdynamics: 20.1% (PE9.71)

MMSV: 21.7% (PE13.3)

QES: 14.5% (PE20.87)

Business (FYE 2021)

Development and manufacturing of machine vision equipment and provision of related products and services.

(Use of product: optoelectronics, solar cells, discrete components and ICs, as well as used in vision guided robotic equipment)

Revenue by Geo

Malaysia: 24.42%

China: 73.45%

Others: 2.13%

Fundamental

1.Market: Ace Market

2.Price: RM0.34

3.P/E: 15.19 @ RM0.0224

4.ROE(Pro Forma III): 12.45%

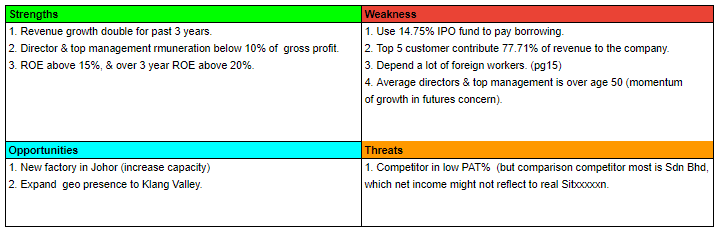

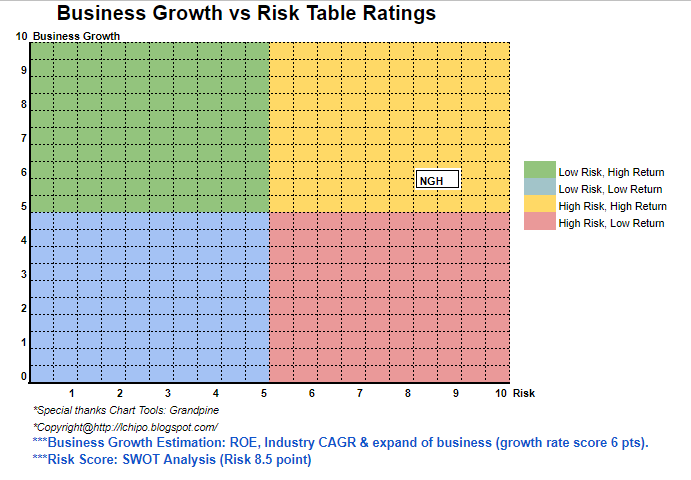

5.ROE: 17.99%(FYE2022), 15.88%(FYE2021), 41.05%(FYE2020), -10.11%(FYE2019)

6.Net asset: RM0.18

7.Total debt to current asset after IPO: 0.32 (Debt: 23.244mil, Non-Current Asset: 35.224mil, Current asset: 72.111mil)

8.Dividend policy: no formal dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FPE 30Jun, 6mths): RM27.358 mil (Eps: 0.0112),PAT: 19.00%

2021 (FYE 31Dec): RM47.264 mil (Eps: 0.0180),PAT: 17.64%

2020 (FYE 31Dec): RM24.927 mil (Eps: 0.0039),PAT: 6.08%

2019 (FYE 31Dec): RM20.660 mil (Eps: -0.0092),PAT: -20.91%

***EPS here used cal based on 468mil shares (prospecture book use 385mil shares, pg15)

Operating cashflow vs PBT

2022: -15.73%

2021: 27.6%

2020: 271%

2019: -92.37%

Major customer (2022)

1. Shenzhen Brightsemi Technology Co., Ltd./China: 43.1%

2. Customer B/China: 20.52%

3. Dominant Opto / Malaysia: 13.76%

4. Shanghai Xingyin Electronic Technology Co. Ltd./China: 5.56%

5. Customer group A/ China and Malaysia: 5.55%

***total 88.49%

Major Sharesholders

Goon Koon Yin: 21.51% (direct)

Wong Yih Hsow: 21.51% (direct)

Jennie Tan Yen-Li: 2.48% (direct)

Tan Oon Pheng: 2.48% (direct)

MTDC (Khazanah wholly-owned subsidairy): 23.47% (direct)

Directors & Key Management Remuneration for FYE2022 (from Revenue & other income 2021)

Total director remuneration: RM1.522mil

key management remuneration: RM0.904mil - RM1.10mil

total (max): RM2.622mil or 13.32%

Use of funds

1. Repayment of bank borrowings: 20.88%

2. R&D expenditure: 27.85%

3. Marketing activities: 2.96%

4. Working capital requirements: 37.17%

5. Listing Expenses: 11.14%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a sunrise industry IPO. However semicond industry is a cyclical industry, current situation is semicond turning into oversupply, the industry will get back to better after oversupply over turn into supply shortage.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter

result release. Reader take their own risk & should do own homework to follow up every quarter

result to adjust forecast of fundamental value of the company.

Overall is a sunrise industry IPO. However semicond industry is a cyclical industry, current situation is semicond turning into oversupply, the industry will get back to better after oversupply over turn into supply shortage.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter

result release. Reader take their own risk & should do own homework to follow up every quarter

result to adjust forecast of fundamental value of the company.