Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 12/12/2022

Close to apply: 30/12/2022

Balloting: 04/01/2023

Listing date: 12/01/2023

Close to apply: 30/12/2022

Balloting: 04/01/2023

Listing date: 12/01/2023

Share Capital

Market cap: 788.094mil (will depend on final IPO price)

Total Shares: 2.0739bil shares

Industry CARG

Forecast M'sia EMS industry 2022-2027 CARG: 10.3%

Competitor comparison

NGH: 7.8% (IPO PE11.9)

ATAIMS: -1.9% (PE-6.74)

Aurelius: 6% (PE30)

PIE: 5.9% (PE16)

SKPRES: 7.5% (PE14.51)

SMT technologies: 3% (GE, PE12)

VS: 6% (PE21.2)

NGH: 7.8% (IPO PE11.9)

ATAIMS: -1.9% (PE-6.74)

Aurelius: 6% (PE30)

PIE: 5.9% (PE16)

SKPRES: 7.5% (PE14.51)

SMT technologies: 3% (GE, PE12)

VS: 6% (PE21.2)

Business (FYE 2022)

EMS provider focusing on the assembly and testing.

(a) electronic components and products to produce completed PCBs, semi-finished subassemblies and fully-assembled electronic products.

(b) semiconductor devices.

Revenue by Geo

Msia: 74.4%

Others: 25.6%

Fundamental

1.Market: Ace Market

2.Price: RM0.38

3.P/E: 11.9 @ RM0.0318

4.ROE(Pro Forma III): 19.90%

5.ROE: 38.20%(FYE2021), 27.37%(FYE2020), 6.16%(FYE2019)

6.NA after IPO: RM0.16

7.Total debt to current asset after IPO: 0.84 (Debt: 457.459mil, Non-Current Asset: 248.833mil, Current asset: 544.138mil)

8.Dividend policy: no formal dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 30Jun, 6mths): RM426.002 mil (Eps: 0.0159),PAT: 7.8%

2021 (FYE 31Dec): RM760.870 mil (Eps: 0.0276),PAT: 7.8%

2020 (FYE 31Dec): RM566.246 mil (Eps: 0.0148),PAT: 5.4%

2019 (FYE 31Dec): RM325.998 mil (Eps: 0.0025),PAT: 1.6%

Operating cashflow vs Profit before Tax (amended)

2022: 13.37%

2021: 46.19%

2020: 139%

2019: -ve

Major customer (2022)

1. Company A (Fully-assembled electronic products): 54.8%

2. Company B (Fully-assembled electronic products): 10.5%

3. Robert Bosch Power Tools Sdn Bhd (Completed PCBs): 9.2%

4. Company C (Completed PCBs): 5.6%

5. Company B (Completed PCBs): 2.9%

***total 83%

Major Sharesholders

Ooi Eng Leong: 57.8% (direct)

Tan Ah Geok: 7.2% (direct)

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM2.783mil

key management remuneration: RM1.45mil - RM1.70mil

total (max): RM4.483 mil or 7.488%

Use of funds

1. Purchase of machineries and equipment: 3.6%

2. Working capital requirements: 29.2%

3. Repayment of bank borrowings: 63.8%

4. Listing Expenses: 3.4%

1. Purchase of machineries and equipment: 3.6%

2. Working capital requirements: 29.2%

3. Repayment of bank borrowings: 63.8%

4. Listing Expenses: 3.4%

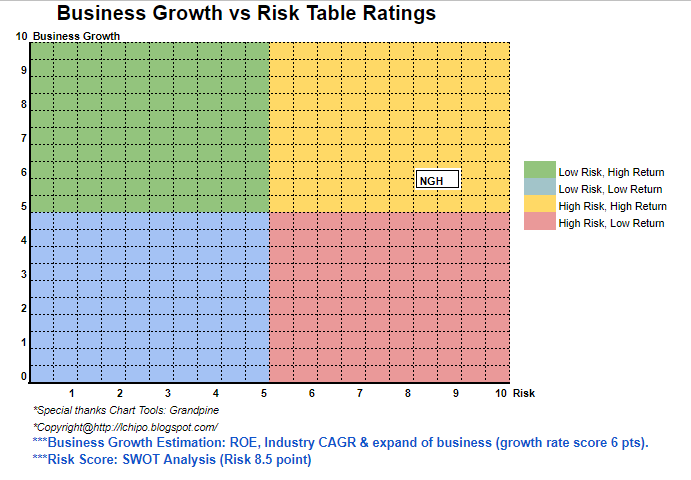

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a low net profit margin industry. The operating cashflow vs PBT drop below 20%, & risk of highly depend on foreign worker. Hence, this IPO will category into high risk category area for rating. (Amended)

Overall is a low net profit margin industry. The operating cashflow vs PBT drop below 20%, & risk of highly depend on foreign worker. Hence, this IPO will category into high risk category area for rating. (Amended)

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.